Leprechauns in the Accounts, Phantom FDI & No Tax on IFSC Traffic – Choices for Ireland!

ThePlatform.ie – Ireland’s Solutions Resource.

By Jim Miller. 27th Sept. 2020

This narrative is not to criticise individuals; This piece is to explain as best I can, the benefit or other to the Irish public, as a whole, of the near total obsession of “official Ireland” with Foreign Direct Investment, and a willingness to be blind to the activities in the IFSC. Most people just do their job, and their knowledge of the job, is based on their ”need to know”. However, many, if not most individuals are, at sometime, called upon to stand by their own integrity, and that sometimes calls for individuals to object to ”the job” or even to walk away from it. Fixing any system, is dependent on individual integrity, amongst other things.

There was a time when the IFSC didn’t exist. Back then most people owned their own houses and weren’t burdened by large debt. Today, as per an RTE reporter a couple of weeks ago, Ireland Inc. is now the tenth most attractive corporation in the world for FDI. One might well ask if there is a connection between the IFSC and FDI. I would say, very much so. However, therein lies a big mystery. Traffic through the IFSC, doesn’t always yield a ”road tax” for the benefit of Irish people, a fact well explained in the TWZ report of June 2018. That report outlined certain facts about, ”shifted profits”, Ireland Inc. being the recipient/destination, of more than €100 billion in 2015.

It Is Imperative to grasp ”gainful employment” or ”productive enterprise” as opposed to enterprises built on extorting from those productive enterprises, profits beyond the imaginations of average folk. This short commentary, avoids the subject matter of waste ”in the system”. However, it is worth highlighting again, in the context of a housing and homelessness crisis, and in the wake of a massive property price crash, and the onslaught by vultures on innocent folk, etc. Etc., that property prices are generally used as a marker of the ”health of the economy”; that practice is a fundamentally wrong and bad practice, creating a very serious illusion. The economy is very different from ‘the people’. Add to that the role played by large property development companies, in extracting /extorting huge profits from the process of delivering new houses to the market; that extraction /extortion of value, is estimated at approx. €100,000, per house, in too many cases.. It should also be clearly understood, that higher property prices, regardless of the real value for either productive or residential purposes, serve as a major support to the commercial banking industry, thus concealing real levels of insolvency. Some mechanism, must be found and delivered, whereby, house prices are properly related to what average people earn. Fixing the ”economy” is an academic exercise. Fixing peoples lives must be top of the list, but that’s a very different matter to fixing ”the economy”

The Cost To Business, of Doing Business, courtesy of the commercial banking and financial industry, needs to be properly appreciated. Professors Margrit Kennedy and Professor Steve Keen explain, from different perspectives, and show how one element of the “non-productive sector” effectively robs up to 40% of the productive element. Said another way, up to 40% of the cost of everything we all buy, goes to the banking industry, so, what or who are we working for? But then there is FDI and the wider financial industry, which, since the ending of Glass-Steagall in the late 1980s, has been on steroids, so to speak, cultivating the derivatives market, a market deemed illegal while Glass-Steagall was in vogue, but is now ”legal and unrelatable”. Thus, in 2020, there are the approx. $1.5 quadrillion of derivatives, which have very little if any foundation whatever. This might explain why the ”overnight rate” of interest, went to 10% last October, and the US Fed issued $6.5 trillion in a few months since Oct 2019, and it might explain to some degree why HSBC shed 10,000 jobs, also last fall, in one day.

The Primary Question here, is, ‘Cui bono”, who benefits from FDI, and even what constitutes “foreign”. Ask yourself if you might be effectively, a foreigner in the eyes of Ireland Inc., the latter being a corporation, to which you might be giving allegiance, unknowingly at your own expense. What if the Irish taxpayer is a primary source of FDI, via tax supports and other interesting mechanisms of financing so called FDI. What percentage of so called FDI into Ireland, €874bn in 2018, is actually borrowed in Ireland, and what rates of interest? Ask yourself, what is ultimately the difference between corporations like Tesco and Ireland Inc.

Ask Yourself, “what if there were €132bn of ‘activity’ in the Irish economy in 2018, which contributed NOTHING TO THE GROSS NATIONAL INCOME”. Ireland Inc. published GDP and GNI sums for 2018, were €300bn and €168bn, respectively, a significant 44% variation.

Eoin Burke Kennedy, scripted an article, published in the Irish Times, recently. The article deals with a recent CSO report. We should be very grateful for that article, for what it says, and for what it hides in plain sight.

The CSO.’s report showed that 383,000 jobs, in Ireland, are directly linked to FDI, an increase of 28% or 84,000 between 2012 and 2018. Most readers would say fantastic and well done. Lifting the bonnet a little, we see that the manufacturing sector has 94,000 FDI jobs, and the retail sector is the second largest at 91000 jobs. To say these 91,000 retail jobs were ”created” would hide from the innocent reader that these 91000 were at the expense of approx 135,000 jobs already retailing Ireland. Ask yourself, and your T.D.’s and ministers, if 91,000 FDI jobs were funded by you, the taxpayer, to replace approx 135,000 jobs? The net benefit to us all is seriously questionable, and must be assessed alongside the loss of so many small family /retail businesses. When you wonder why we have so few small family businesses and small traders in our streets, “FDI retail” has those jobs, while your children and grandchildren, whom you ‘educated’, are in the US, Australia and Canada.

After Retail and Manufacturing, one must presume that the balance of the FDI jobs, 198,000 are in “services”, presumably financial services, most of which contribute nothing to GNI.

It gets better, or worse, depending on perspective.

The Average Salary earned in Ireland (according to CSO report) by people with FDI sourced /linked jobs, is €54,000 p/a. Whereas, non FDI jobs yield an average of €37,000. One might think FDI fantabulous with such an outcome in incomes. I ask the reader to enlighten this author, as to the percentage of employees working in those FDI retail jobs, such as TESCO, ALDI, LIDL etc. etc., who earn €54,000. I would suggest that the vast majority of these FDI jobs in retail Ireland, via multinational outlets, are yielding on average, closer to €20,000 than €54,000. Maybe someone can solve this riddle for me.

How many Irish people emigrated after the engineered crash of 2008?, was it a quarter or half a million? I ask the reader to fully evaluate the above facts and queries.

Back in Feb 2009, a certain politician of high ranking, boasted at a local venue in Donegal, about all the jobs Tesco would ”create” as it opened its network of nearly 30 depots in the republic. Not one public representative challenged the comments, from which fact, I must deduce that they all agreed with the plan. Of course, planning permissions had to be acquired and that can be tricky at county council level, lest anyone’s toes be walked on. Even the terms of certain planning permissions are worthy reading, as some competitors to certain FDI retailers found themselves in court. I was aware back in 2009, of the generally accepted statistic, that for every job ‘created’ by Tesco, 15 people would lose their jobs; exit how many small traders? Walk the streets of any town today, and witness the hardship endured by the few small family owned businesses to survive, present new anti trading streets, and parking fines which don’t apply in outlying town-shopping zones.

But, but, there is more to read from Eoin Burke Kennedy’s article. In 2018, there were €874bn of FDI in Ireland. Wow, but that seems simply mega. Where did that go? Well, in fact, only 24%, or €212bn was “real” – the balance being explained as ”pass through investment, reverse investment (involving subsidiaries making payments back to parent company), intellectual property (IP) and aircraft leasing assets”. Remember, that the €874bn FDI was almost 3 times the GDP at €300bn.

Now It Gets Even More Interesting: there were 84,000 extra FDI jobs ‘created’ over the 6 years 2012 to 2018. Overall, that’s an average of 14,000 jobs per annum. It is easy to see where the FDI retail jobs were “created” perhaps. However, this would suggest that the €212bn “real FDI” in 2018, actually created about 14,000 jobs, across the full spectrum of FDI linked jobs, in manufacturing, retail and services. That also suggests that each job cost approx €15 million? The average salary was €54,000 in 2018. I am to ask if each one of these FDI jobs produce/d on an annual basis, sufficient Euro value to repay the investment of €15 million plus salary and other costs of production. In many, if not most enterprises, 3 years might be ambitious to see a full return on investment, but even at 7 years, the output would need to be in excess of €2 million per annum? Is this credible, for each of 14,000 employees, when in fact some are in the retail sector. Are you, the taxpayer, funding some of this “investment”, and if so, how much. Explanations required and deserved by the public.

Mad Query. What if the entire €874bn FDI in 2018, was to be married off to the approx 14,000 FDI linked jobs in 2018? Is that not approx €62+ million per job, including jobs in retail? There would need to be a real gold rush somewhere.

Based on that 2018 figure of a total of €874bn FDI investments in Ireland, I wonder if The minister for finance, or the secretary of finance, would have time to explain to us all, where the balance of €662Bn went to, and who benefited.? But I guess that would be like asking certain people, where the missing trillions ended up as the TRIPLE TOWERS CAME SO RAPIDLY TO EARTH on 9/11. Remember, that €662bn was just for 2018.

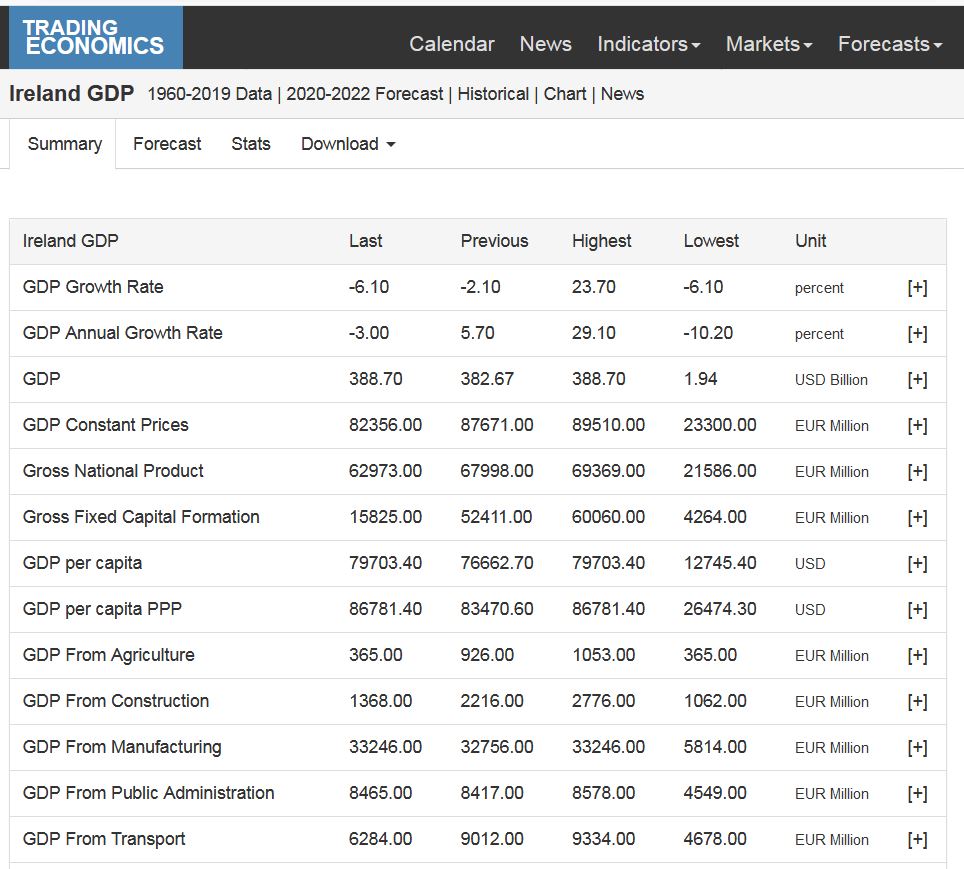

Please Try To Digest the following published data. The 2018 GDP was 300bn, as against €168bn for GNI, a 44% variation. Now alongside that piece of data, was the presentation “as fact” that Agriculture contributed 1.2% to GDP; i.e. €3.6 billion out of €300bn. (See Annex ‘A’, where Agriculture is pitched at less than €700 million GDP, out of a total €300bn, whereas transport is pitched at approx 12 times that amount.) Industry and manufacturing contributed 38.6% of the €300bn, GDP. That detail informs us that Agriculture, industry and manufacturing, contributed 39.8% (approx €120bn) of the total GDP, whilst SERVICES contributed the balance of €60.2%. I am concluding that the so-called SERVICES, made up all the 44% variation between GDP and GNI, with that 44% variation, of €132bn, contributing nothing to GNI.

There Are Approx. 2.2 Million People Employed officially, in Ireland, 383,000 of whom are ‘linked’ to FDI. This suggests that approx 2 million employees produced €168bn GNI, while 198,000 employees delivered €132bn of ”services”, as part of Ireland Inc.’s GDP, but contributed nothing whatever to Gross National Income. Herein lies another falsity, by extension. Most of the world knows that Ireland’s leprechaun economy is in financial services, thus misrepresenting internationally, Ireland Inc.’s GDP, @ €300bn in 2018. Irish Government debts are being represented as a % of GDP. Government debts of €210bn as opposed to GDP of €300bn, looks OK. However, when Government debt is compared to Gross National Income, things look very different; i.e. €210bn versus, €168bn. Those leprechauns are difficult to see in daylight.

IFSC living by its own rules and not in the real world, by Elaine Byre Published In 2012, outlined how a 1% tax on the trades in IFSC, would yield about €50bn per annum. Nice tidy sum that, for 2011, which in 2020, would probably be €75bn.

Then again why expect activities in IFSC to yield tax, when, sure? no one pays tax in Ireland; no income tax for anyone, no vat, no car tax, no water tax, no rates, no property tax; you wish. Surely, it would be so unfair to tax the IFSC at even 1%. My question is, what do the contracts for the IFSC operators actually say, and who signs these contracts on your behalf? You all remember the ‘Apple’ worth €13 billion, which still hasn’t found its permanent home; it might even have rotted by now. However, I ask the reader to note what David Mac Williams said in Oct of 2016,on RTE radio, that according to his estimates the multinationals were paying about €4bn in tax, out of €12bn annually. Did that €13bn apple just turn into an €80bn apple over about 10 years? Are you struggling with a mortgage? Struggling to afford a family? Struggling to know why you have to work two and three jobs to keep a household, when this was easily enough done 50 years ago, on one household salary? You are entitled to have your minister and local TD’s explain all this; if they cannot explain then they should vacate their positions. Either everyone pays some tax or no one pays any tax, fair play being good sport.

I am of the opinion that the secretary of Dept of Finance, and the Minister for same, and some others, should be called to the Dáil Finance Committee to explain all this in detail. The revenue top-cat might also be required.

Funding Debt. A certain financial strategist, published some months ago, data, which I cannot fully verify. However, that data as published, supposedly from World Bank data, indicates that Ireland Inc.’s debts cost 10.8% of GNI to fund; i.e. 10.8% of €168bn in 2018. That’s approx €20 billion, out of a total tax take of approx €50bn. This begs so many questions. Mostly however, it proves some of the actual cost of the 2008 engineered crash. The published claims have not been refuted, to the best of my knowledge. Would the reader consider, or even be allowed to commit 40% of net income to a mortgage payment? I guess this is another reason we have 35-year mortgages, which should be outlawed.

A Report, Published In Early 2018, evaluated FDI in the Spanish economy. The conclusion was as follows; ”FDI IN THE SPANISH ECONOMY, CONTRIBUTED NOTHING TO THE GDP”

What if the same applies in Ireland? No proper analysis of the true value of FDI in this country has ever been seen by this writer. The past 50 years of FDI and EEC/EU control over the Irish psyche, has catered for the gifting of most every native and national resource to whosoever presented an illusion of value, and perhaps some ”encouragement” to key people in key positions? But for the rising of the people against the sell off of our water resources, the latter would have also been given away, and the figure mentioned was €11bn. In the context of national and native assets, minerals etc., I am to ask if the 2009 Land and Conveyancing Act, had any impact on ”allodial”, and if so, why, and for whose benefit?

What are the Impacts of FDI Obession? Firstly and fore mostly, is the down grading of Irish and native interests. That downgrading has led to the effective export of 2 generations, at least 0.5 million of young Irish since we joined the EEC. Most Irish people seem to think that the EEC/EU has been great for this country. This writer is of the view that membership of the EEC/EU, rather than gifting us approx €80bn in one manner or other, has in fact, robbed the Irish people of a sum of wealth north of €1.5 trillion, and likely double that. What external influences in this country over the past 50 years, have determined that any and all interests across the world are more important that those of our own people. What was/is the full cost to the Irish people of the 2008 engineered financial crash? What is the full cost of the gifting to the world of Ireland’s phenomenal fishing resources? What mineral resources have been given away?

I suggest it is time for Irish and European people to acknowledge that the plan for ”the new European” as scripted by Coudenhove-Kalergi in 1922, is well on the way to completion. Jean Monnet, the so called father of the EU and also a CIA agent, would surely laugh and chuckle at the success of the second major communist experiment, which is the EU. Rather than develop our own skills and native resources, Ireland Inc. has seen fit to unlawfully gift away most everything to all and sundry, and even to accommodate, via the abuse of our civilian airport at Shannon, the murder of 1 million children in Iraq. The financial crash, over which the ECB and Commission presided with prior knowledge and lots of determination, to bomb ”Dublin” into submission, has cost the Irish people at least €500 billion by way of wealth transfer to vultures and elites, and probably twice that. The gifting of the Irish fishing resources and the native industrial potential in same, cost the Irish people at least another €600bn. What is the financial cost of the 1/2 million+ who were forced to emigrate, and never to return, never mind the human cost. The above costs are courtesy of a total and blind ignorance or complicity, throughout officialdom in Ireland, to understand how the commercial banking industry has been completely red carpeted to extract maximum benefits from Irish people, ever since, and maybe even prior to, the Central Bank Act 1942. My estimate is that net financial/monetary impact of the loss of 1/2 million Irish to foreign lands, was /is in excess of another €1 trillion. What Ireland Inc. acquired for itself was/is €2.2 trillion of “external debt”.

In conclusion, we lost possibly as much as €3 trillion, and we garnered ‘external debts’ of €2.2 trillion…that’s €5.2 trillion….but we have great roads?. The exact reality may not be as outlined above, but let someone prove otherwise. The picture is much worse if one were to value every Irish man and woman’s Birth Cert Trust Fund at €10 million each, or at $1billion each, as suggested by certain researchers. If we were to pursue the logic of the newly reformed national government of the 50 American States, then the total liabilty to the Irish people might reach €12trillion or even €15 trillion.

See Elsewhere On ‘ThePlatform.ie’ Professor Steve Keen explain how those same commercial banks bleed the economy all the time to the tune of 35-40% of the productive element. If the productive element in the Irish economy is represented by the GNI at €168bn (2018), then the maths are simple and startling; this is how wealth is transferred upwards all the time, and how we have the stupid concept of “affordable housing” in an economy dominated by leprachaun type of ‘experts’, selling dud economics to anyone with less than very critical ability. Ask yourself if €80bn in EEC/EU subsidies and road building funds, was a good trade for minimum €1,5 trillion wealth exrtraction, and more likely €3 trillion, depending on how one approaches the issues.

But of Course, a certain Taoiseach, not very well versed in the colours of Irish history, held the view that Ireland will be better off with a million immigrants from wherever, thus facilitating Agenda 21/2030, and the multicultural agenda of those who prefer farming people to farming land, or even 4 legged cattle.

Fundamental To The FDI Obsession, and the gifting of everything national and native to all and sundry, is the very simple fact of the misuse and abuse of “THE CREDIT OF THE NATION”: THIS IS WHAT THE GERMAN PEOPLE FIGURED OUT MORE THAN 200 YEARS AGO. IT IS TIME WE LEARNED AND TOOK BACK INTO THE HANDS OF THE PEOPLE, CONTROL OVER THEIR OWN CREDIT. Sovereign slavery is a contradiction and an oxy-moran. Effective Sovereignty requires economic sovereignty as a sine qua non.

It is extra ordinary and inexplicable that since that Central Bank Act,1942, only one public representative, and no political party, has ever challenged it, despite the fact that it runs directly counter to the Bunreacht of 37. The sole objector was James Dillon, who, during that rigged debate with only 5 or 6 members in the Dáil, obviously knew what was happening, but seemingly no one else ever since has figured it out? 70% of the German banking industry is owned by the people, and works solely for the people. In Aug 2018, the then, and current minister for finance, launched the Gov report on Public/Community banking; it simply said it was too expensive and would add nothing. This writer, requires the same minister and the new government, TO CLEARLY understand, that for €40 per head of population we could have a very strong Sparkasse type community banking model operating here; For less than €100 per head of population over 5 to 10 years, we could have a community/public bank in every county of the 32 counties, with several in the larger population areas. I require the minister to explain how even the larger sum cannot be afforded, never mind the smaller one. I live in the hope that everyone will demand answers from the minister. Explain, Minister; ‘we the people’, deserve some honesty and some clarity as to how you dismiss €40 per head of population over 5 years as too expensive.

Minister, and people all, that is less than €0.70 per month over a 5 year period. Less than €0.90 per month over 10 years would create a sublime model of community banking, serving every family and small business, in every village from Malin Head to Mizen head, and from Inis Mór to lambay.

Of Course the creation of a comprehensive network of community banks, would expose the insolvent commercial banks operating here, as they have been since at least 2005, despite their being bailed out at inestimable cost in wealth transfers to whoever, to the tune of more than €500bn, IMHO. That insolvency was properly and fully explained to the Dáil Finance Committee on 28May 2019, an exposé worthy of everyone’s’ ears and concentration. How many other insolvent entities are allowed trade, or is it just banks?. Of course, insolvent banks require exorbitant property prices to fudge an illusion of solvency and viability. Property prices are not and should not be used as a guide to the general welfare of families and communities. The concept of “affordable housing” must be undone. If 90+ % of housing is not affordable to ordinary working people, then why does it exist?

Reader Be Aware that money lent (by way of so called deposit) to an insolvent bank, is not safe, as it is not yours any more, and much of the $1.4 quadrillion derivatives have primary call on “your money”. Your so called deposit, which is in fact an “unsecured loan” to that insolvent bank.

These Community Banks, would operate like the Sparkasse, to the highest levels of transparency and ethics, no securitisation, no speculation, with the mission “to make business” work, and never to be bought or sold. That business would be SME business and family business, not FDI enterprise. In the context of a proper community banking model, indigenous Ireland can thrive; absent same, this government like each Government since 1992 will pursue with their international and multinational allies that UN Agenda, 21/2030, which strives towards RURAL DEPOPULATION, URBANISATION AND AN END TO PRIVATE PROPERTY. The ongoing, never ending bleeding of peoples energies and wealth, to the commercial banking industry, is, perhaps, best reflected today in the requirement for sponsorship in every sporting organisation, and even in RTE. Even the GAA/CLG has resorted to accepting the renaming of its stadia with the names of large sponsors. It seems obvious now, that Croke Park stadium name, will soon be flogged off to the highest bidder regardless of private or commercial agenda. In recent times the GAA has accepted sponsorship to advertise the Gardasil vaccine; this is fundamentally wrong, even scurrilous, for so many reasons. The largest amateur sports association in the world, has finally capitulated to the financial sponsors, thus insulting the several generations who built the association and its facilities with hard work and personal endeavour over almost a century and a half.

Conclusion/Choices/Authority

Commercial banks and FDI can thrive aplenty, in a restricted manner, alongside community banks, but communities and families are just driven to impoverishment and cannot survive, never mind thrive without community banks. What if the wealth transfer, of up to 90% of peoples’ output/productivity is sucked upwards to the 1% through the commercial financial industry. The Minister’s spoof that community banks would prove too expensive, is simply wrong. The cost to the general public, of payments in all forms by the state, and the banking costs associated with running semi state organisations, county councils, schools, Universities, sports organisations etc. etc. etc. channelled properly through a community banking network would probably pay the salaries of the entire community bank network, rather than subsidising insolvent parasitic commercial banks, which have only one function which is to bleed the public of 35/40% of everything we all buy. That network of community banks, would create balance for communities, SMEs and families, by removing from the commercial banks, the total and absolute control over most all financial transactions across the country. The commercial banking industry, does as it does because “we the people” allow it to do so; for them it is just business. “we the people” have choices. Its you /us or them. Make your choice. If you want banks to work for you, then demand same….don’t ask….demand; you have that authority, and the credit of the nation is yours to claim and make work for you and yours.

Addendum. Recently, the decision re Apple’s €13bn has been made. This raises many questions, but a couple of fundamental ones. Again who will benefit. Remember what is asked above. Firstly, should the €13 billion not be read as €80bn, not all from Apple? Secondly the matter of the true value/cost of €13bn needs to be estimated in some detail. Thirdly, how will the €13bn be dealt with? Will it be repatriated or spent in Ireland? If spent in Ireland, who will determine the spend. What multiplier will apply; what if it is a multiplier of 5 or even 8? Whether its €13bn or €80bn, is it not tax which wasn’t paid, so who made up the difference, and should we not have this money back. I suggest people demand full and adequate explanations, without the fudge. Just 2% of the €13bn would create a wonderful and comprehensive network of community banks; can the minister still say it would be “too expensive”, over 5 years. This would rebalance business potentials in this country, by putting local first and allowing it to survive and thrive, absent the begging bowl to EU, and absent recurring forced emigration. Then we could offer to invite to come back home, one of the 70 million Irish from across the world.

By Jim Miller.

Chairman of the PBFI (Public Banking Forum of Ireland)

Contact Jim Miller at spiritofeireann@hotmail.com

Annex A.

Ireland GDP

The gross domestic product (GDP) measures of national income and output for a given country’s economy. The gross domestic product (GDP) is equal to the total expenditures for all final goods and services produced within the country in a stipulated period of time. This page provides the latest reported value for – Ireland GDP – plus previous releases, historical high and low, short-term forecast and long-term prediction, economic calendar, survey consensus and news. Ireland GDP – actual data, historical chart and calendar of releases – was last updated on October of 2018.

Ireland GDP Table & Description by Trading Economics.

Referenced Articles & Quotes:

- Elaine Byrne: IFSC living by its own rules and not in the real world by Elaine Byrne, May 2012

- TWZ Report

- More than a third of Irish FDI is ‘phantom’ investment – CSO by Eoin Burke-Kennedy, May 6, 2020

- Interest – Professor Margrit Kennedy.

- Professor Steve Keen on why the recovery is doomed.

- Does Foreign Direct Investment Generate Economic Growth? A New Empirical Approach Applied to Spain Jorge Bermejo Carbonell & Professor Richard A. Werner

- IFSC photo by Kaihsu Tai

- Leprechaun image by dulemba.blogspot.com